Organizing financial resources effectively is one of the most critical responsibilities within any enterprise. Securing budget approval often requires more than just a list of desired expenditures; it demands a clear demonstration of value and strategic alignment. When leaders present financial requests, they face scrutiny regarding cost, timing, and expected returns. The Business Motivation Model (BMM) provides a structured framework to articulate these needs. By mapping organizational goals to specific capabilities and resources, teams can construct a compelling narrative for investment. This approach transforms budgeting from a negotiation into a strategic alignment exercise.

This guide explores how to leverage the Business Motivation Model to analyze Return on Investment (ROI) and secure necessary funding. It focuses on logical justification, clear metrics, and stakeholder engagement without relying on specific software tools or generic promises. The objective is to provide a robust methodology for financial justification rooted in organizational motivation.

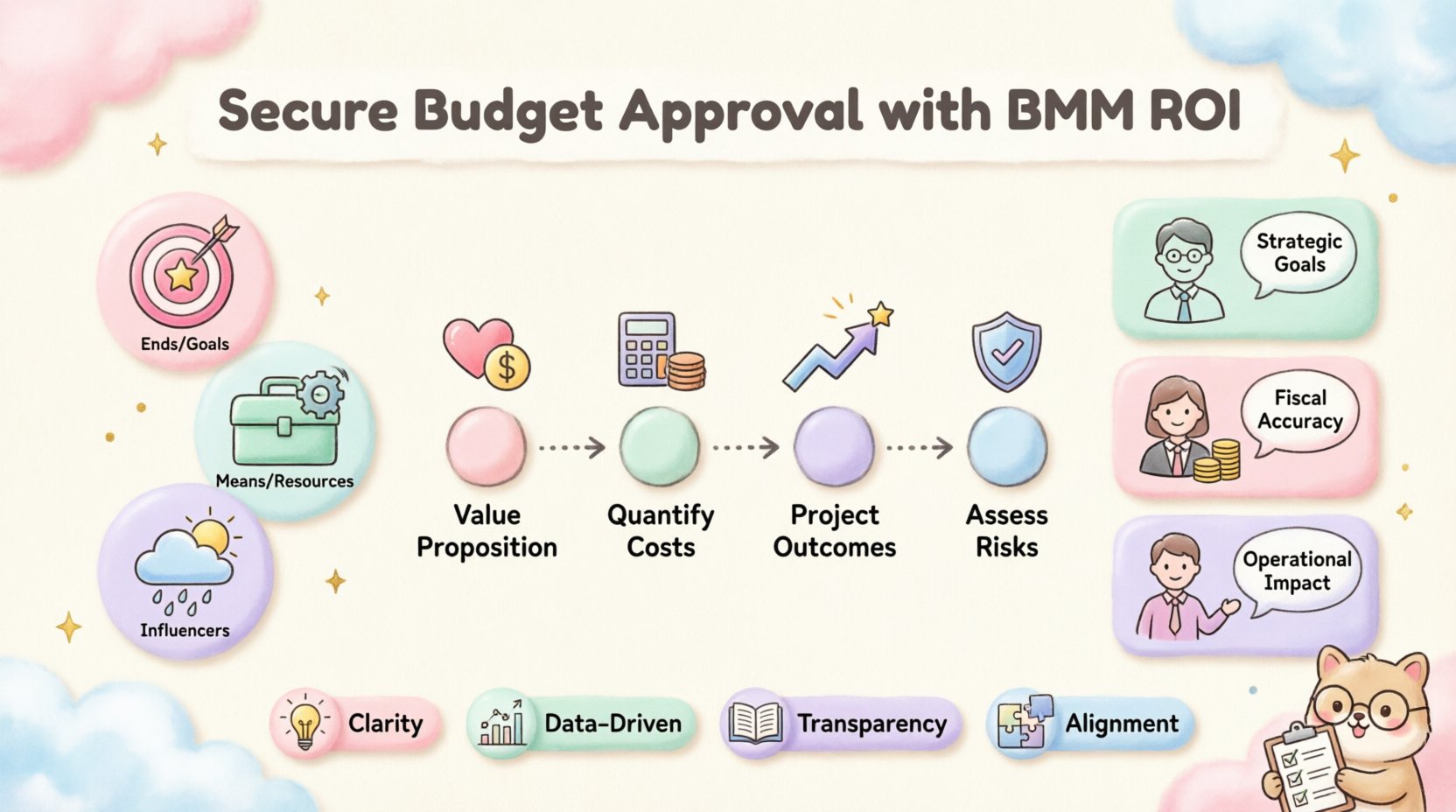

Understanding the Core Components of the Business Motivation Model 🧩

Before diving into financial analysis, it is essential to understand the foundational elements of the Business Motivation Model. BMM is a conceptual framework designed to describe how an enterprise achieves its desired outcomes. It breaks down the complex reality of business operations into manageable, interrelated components. These components help in visualizing the path from high-level strategy to daily execution.

For the purpose of budget justification, three primary categories are most relevant:

- Ends: These represent what the organization wants to achieve. They include strategic goals, objectives, and intentions. In a budgeting context, ends define the “why” behind the spending.

- Means: These are the capabilities, processes, and resources required to achieve the ends. This includes technology, personnel, and infrastructure.

- Influencers: These are external or internal factors that impact the success of the means. They can be market conditions, regulatory changes, or competitor actions.

When analyzing ROI, the connection between Ends and Means is the primary focus. The budget request usually targets the acquisition or enhancement of Means. To justify this, one must demonstrate how those Means directly support the Ends.

The Relationship Between Strategy and Investment

Many budget proposals fail because they focus solely on the cost of the Means without adequately connecting to the Ends. A common mistake is to request a new software platform without explaining which strategic goal it supports. BMM corrects this by forcing the requester to explicitly link the investment to a specific objective.

Consider the following structure:

- Goal: Increase customer retention by 15% over the next fiscal year.

- Means: Implement a new customer relationship management system.

- ROI Analysis: Calculate the cost of the system against the projected revenue gain from the retention increase.

This logical chain makes the budget request defensible. It shifts the conversation from “how much does this cost?” to “how much does this value contribute?”

Integrating ROI Analysis within the BMM Framework 💰

Return on Investment is a standard metric, but applying it within the context of BMM adds depth. Standard ROI calculations often look at immediate financial returns. However, BMM allows for a broader view that includes strategic value and risk mitigation. This section outlines how to structure the analysis to satisfy both financial auditors and strategic planners.

The integration process involves four key phases. Each phase ensures that the financial data supports the motivational intent of the project.

Phase 1: Defining the Value Proposition

Value is subjective and varies by stakeholder. A CFO looks at cash flow, while a CTO looks at technical debt reduction. Using BMM, you map the specific value to the specific stakeholder’s interests.

- Financial Value: Direct revenue increase, cost reduction, or efficiency gains.

- Strategic Value: Market positioning, brand reputation, or compliance readiness.

- Operational Value: Reduced downtime, faster processing times, or improved employee satisfaction.

By categorizing value, you ensure the ROI analysis addresses multiple dimensions of organizational motivation. This prevents the analysis from being too narrow.

Phase 2: Quantifying the Means

This phase involves determining the total cost of ownership for the proposed Means. It is not just the purchase price. It includes implementation, training, maintenance, and potential downtime during transition.

A comprehensive cost breakdown should include:

- Capital Expenditures (CapEx): One-time costs for acquisition.

- Operational Expenditures (OpEx): Recurring costs for support and licensing.

- Hidden Costs: Training time, productivity loss during setup, and integration labor.

Transparency here builds trust. Hiding costs in the “hidden” category often leads to budget overruns later, which undermines the initial approval.

Phase 3: Projecting the Outcomes

Once costs are defined, you must project the outcomes based on the Ends. This requires data and reasonable assumptions. Avoid overly optimistic projections that are difficult to defend.

Key metrics to consider include:

- Time to Value: How long until the investment starts paying back?

- Break-even Point: When do cumulative returns equal cumulative costs?

- Net Present Value (NPV): The current value of future cash flows adjusted for time.

Using BMM helps justify longer time horizons. If the End is a long-term strategic shift, the ROI timeline should reflect that maturity rather than expecting immediate quarterly returns.

Phase 4: Assessing Influencers and Risks

BMM explicitly accounts for Influencers. In budget terms, these are risks. Every budget request carries risk. The analysis must acknowledge how external factors could alter the ROI.

- Market Volatility: Could a shift in the market reduce the expected revenue?

- Regulatory Changes: Might new laws increase compliance costs?

- Technology Obsolescence: Could the technology become outdated faster than expected?

By documenting these risks, the proposal shows thorough planning. It indicates that the team understands the environment in which the investment will operate.

Structuring the ROI Analysis for Stakeholders 📊

Different stakeholders require different levels of detail and different types of information. A single document rarely satisfies everyone. Using BMM, you can tailor the presentation to the specific Motivations of each group. This section outlines how to structure the information for maximum impact.

The Executive Summary for Leadership

Senior leadership often lacks time for deep technical details. Their primary motivation is organizational health and strategic alignment. Their view should focus on the “Ends” and the high-level ROI.

Key elements for this audience:

- Clear statement of the strategic goal being supported.

- Summary of total investment required.

- High-level return projection (e.g., 3-year NPV).

- Top three risks and mitigation strategies.

The Financial Detail for the CFO

The Chief Financial Officer needs to verify the numbers. Their motivation is accuracy, compliance, and fiscal responsibility. The analysis must be granular and auditable.

Key elements for this audience:

- Itemized cost breakdown (CapEx vs. OpEx).

- Sensitivity analysis showing best-case and worst-case scenarios.

- Cash flow impact over time.

- Comparison against similar historical projects.

The Operational Detail for Department Heads

Department heads care about implementation and daily impact. Their motivation is operational continuity and resource availability. They need to know how the budget affects their team.

Key elements for this audience:

- Implementation timeline and milestones.

- Training requirements for staff.

- Impact on current workflows.

- Support and maintenance commitments.

Creating a Comparative Matrix for Decision Making 📋

When multiple budget requests compete for limited resources, a comparative matrix is essential. This tool allows decision-makers to evaluate options side-by-side based on BMM criteria. It removes emotion from the selection process.

The following table demonstrates how to structure such a comparison. It aligns BMM elements with financial metrics.

| Proposal | Strategic Goal Alignment | Total Investment | Projected ROI (3-Year) | Implementation Risk | Strategic Value |

|---|---|---|---|---|---|

| Project Alpha | High (Core Strategy) | $500,000 | 25% | Low | Market Expansion |

| Project Beta | Medium (Support) | $200,000 | 15% | Medium | Efficiency |

| Project Gamma | Low (Nice-to-have) | $100,000 | 10% | Low | Employee Morale |

This table highlights the trade-offs. Project Alpha has the highest strategic value but also the highest cost. Project Gamma is cheap but offers less strategic impact. This visual aid helps leadership prioritize based on their current strategic focus.

Common Pitfalls in Budget Justification ⚠️

Even with a solid framework, errors can occur during the budgeting process. Awareness of common pitfalls helps in avoiding them. These mistakes often stem from a lack of alignment between the Means and the Ends.

Pitfall 1: Overestimating Benefits

It is tempting to project the best-case scenario as the standard. This leads to disappointment when actual results fall short. To avoid this, use conservative estimates for revenue and optimistic estimates for efficiency gains only if supported by data.

Pitfall 2: Ignoring Opportunity Costs

Every dollar spent on one project is a dollar not spent on another. Budget proposals should acknowledge what is being sacrificed. If Project A is funded, what project is deferred? Highlighting this shows a mature understanding of resource constraints.

Pitfall 3: Focusing Only on Initial Costs

Many proposals focus heavily on the initial purchase price and ignore the long-term operational costs. This creates a “false economy.” A cheaper tool that requires more maintenance may cost more over five years. Always project the full lifecycle cost.

Pitfall 4: Neglecting the Influencers

Assuming the market environment will remain static is risky. If the proposal relies on current market conditions, it must include a contingency plan for market shifts. BMM encourages identifying these influencers early.

Implementing the Analysis in Practice 🛠️

How do you move from theory to practice? The following steps outline a practical workflow for preparing a BMM-based budget proposal. This workflow ensures all bases are covered before the request is submitted.

- Step 1: Identify the Primary Goal. Write down the specific business outcome you want to achieve. Make it measurable.

- Step 2: Map the Required Capabilities. List the specific changes in capability needed to reach that goal. This is your “Means” list.

- Step 3: Assign Financial Values. Attach cost estimates to each capability. Be precise and itemized.

- Step 4: Calculate the Return. Estimate the financial or strategic return for achieving the goal. Link it directly to the capabilities.

- Step 5: Assess Risks. Identify factors that could prevent the goal from being met. Plan for them.

- Step 6: Prepare Stakeholder Versions. Create tailored versions of the proposal for different audiences (Finance, Leadership, Operations).

Continuous Review and Adaptation 🔄

Budgeting is not a one-time event. It is a continuous cycle. Once a budget is approved, the BMM framework remains useful for tracking performance. Regular reviews ensure that the Means are still driving the Ends as expected.

Key activities during the review phase include:

- Tracking Actuals vs. Projections: Compare the real ROI against the projected ROI. Analyze variances.

- Re-evaluating Influencers: Have market conditions changed? Do new risks need to be added to the plan?

- Adjusting the Means: If the original capabilities are not delivering value, consider pivoting to different capabilities.

- Updating the Goal: Sometimes, the strategic goal itself may shift. The budget should align with the current reality, not the past plan.

This adaptability is a strength of the BMM approach. It treats the budget as a living document that supports the evolving organization, rather than a static contract.

Final Considerations for Sustainable Growth 🌱

Securing budget approval is a significant milestone, but it is not the end of the journey. The true value lies in the execution and the realization of the intended outcomes. Using the Business Motivation Model provides a robust foundation for this process.

By focusing on the alignment between Ends and Means, organizations can make better investment decisions. This alignment ensures that money is spent on things that actually move the needle. It reduces waste and increases the likelihood of success.

Remember the following points for future requests:

- Clarity is Key: Ensure the goal is clearly defined and understood by all parties.

- Data Drives Decisions: Use historical data and realistic assumptions to support claims.

- Transparency Builds Trust: Be open about risks and costs.

- Alignment Drives Approval: Connect every dollar to a strategic objective.

The Business Motivation Model offers a disciplined way to approach financial justification. It moves the conversation beyond simple cost-cutting to value creation. When applied correctly, it turns budget requests into strategic proposals that are difficult to reject.

Adopting this framework requires effort upfront. It demands a deeper understanding of the organization’s goals and the resources required to meet them. However, the payoff is a more resilient budget process and a clearer path to organizational success. By treating budgeting as a strategic alignment exercise, teams can secure the resources needed to thrive in a competitive environment.

Ultimately, the goal is to create a culture where financial decisions are made with clarity and purpose. The BMM provides the structure to achieve this. It ensures that every investment is justified by a clear motivation and a measurable return. This discipline is essential for long-term stability and growth.

As you prepare your next budget proposal, consider how the Business Motivation Model can enhance your analysis. Use the framework to map your goals, define your means, and quantify your value. By doing so, you position your request not just as a cost, but as a catalyst for the organization’s future success.